Note: You can find the charts & graphs for the Big Story at the end of the following section.

_________________________

More opportunities for buyers in a less competitive market

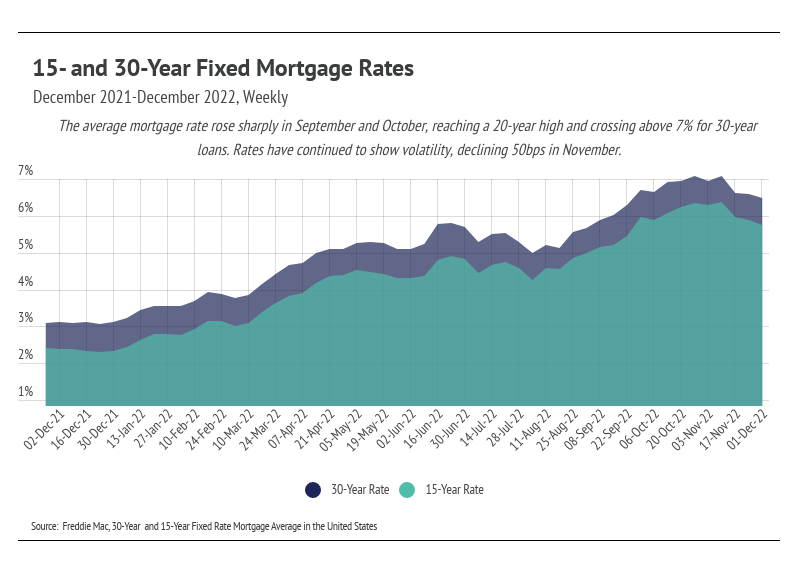

Buyers acted in their financial interest remarkably well between 2020 and 2022, evidenced by the type of financing buyers used to purchase homes during that period. The average 30-year mortgage rate reached record lows in the third quarter of 2020, dipping below 3% for the first time ever. The super-low cost to borrow priced more potential buyers into the market because of the massive increase in affordability. For example, if you can afford the monthly payments on a $500,000 loan at 6% (~$3,000/month), then you can afford a $700,000 loan at 3% (~$3,000/month). Homebuyers, in a sense, could afford more home, so conventional loans rose to the highest level since 2006, and prices rose at the fastest rate in history. Importantly, prices rose quickly, but buyers weren’t getting priced out of the market because of the outsized effect interest rates have on affordability. Financing through conventional loans remained elevated through Q1 2022, which marked a sharp increase in mortgage rates and inflation.

The changing economic environment in Q1 2022 wasn’t lost on cash buyers, either. Inflation was moving higher and depreciating the value of a dollar, which caused all-cash home purchases to jump to the second-highest level on record (just below the all-time high reached in 1988). Buyers’ money was worth more, so spending in the near term had more value. We recognize that cash purchases are far less common, but those who could pay cash chose wisely. We expect all-cash purchases to stay elevated, as mortgage rates will likely remain in the 5-8% range for the foreseeable future. It should come as no surprise that cash purchasers typically have an edge, and that remains true now. However, the typical buyer who finances part of the cost of the home has more opportunity than expected this year.

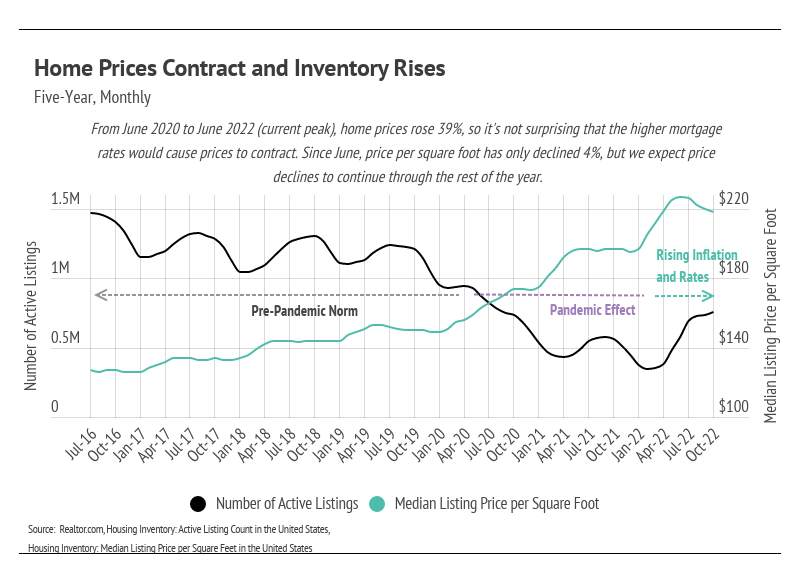

Competition for homes typically softens during the winter months because people focus on the holidays and tend to be less active because of the colder weather and shorter daylight hours. Add in 15- to 20-year-high mortgage rates, prices still near record highs, high inflation, and worries over a recession, and let’s say the competition over homes tends to decline further. This year, sales have dropped every month since January according to the National Association of Realtors, a 32% drop overall. If this trend continues through the rest of the year (current data ends October 2022), which it almost certainly will, 2022 will have about a million fewer sales than 2021. Of course, 2021 had the largest number of sales since 2006, with nearly a million homes sold above the long-term average. With that in mind, it stands to reason that about a million fewer homebuyers than average would be in the market in 2022, especially when considering that financial incentives to buy ended abruptly at the start of this year. We were still surprised to see inventory rise in October after inventory appeared to peak in September.

The housing market has seasonal trends during which home prices and inventory generally rise in the first half of the year and fall in the second half. We will likely have more homes on the market than expected this winter, in a less competitive market, giving buyers a greater chance of finding the right home. Sellers are often buying in conjunction with selling their homes, so more inventory also benefits them.

The U.S. housing market has certainly shifted throughout the year, and we must recognize the current conditions homebuyers and sellers face. Of course, different regions vary from the broad national trends. Take a look below at the Local Lowdown for in-depth coverage of your area. As always, we will continue to monitor the housing and economic markets to best guide you in buying or selling your home.

Big Story Data

The Local Lowdown

-

The San Francisco housing market has cooled considerably in the second half of 2022, a trend that will likely continue through the winter months.

-

The decline in demand has opened more opportunities for buyers in the market this winter.

-

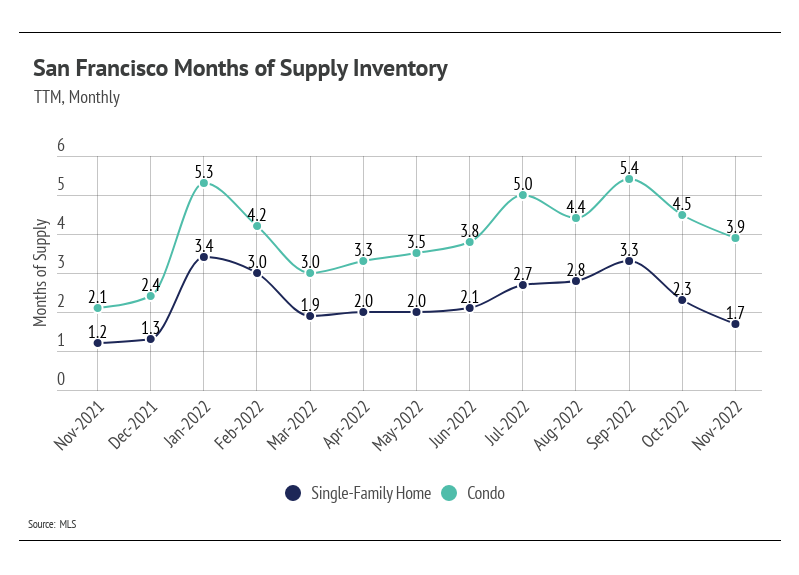

Months of Supply Inventory indicates the market shifted back to a sellers’ market for single-family homes and toward balanced for condos.

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

_________________________

Entering the holiday slowdown

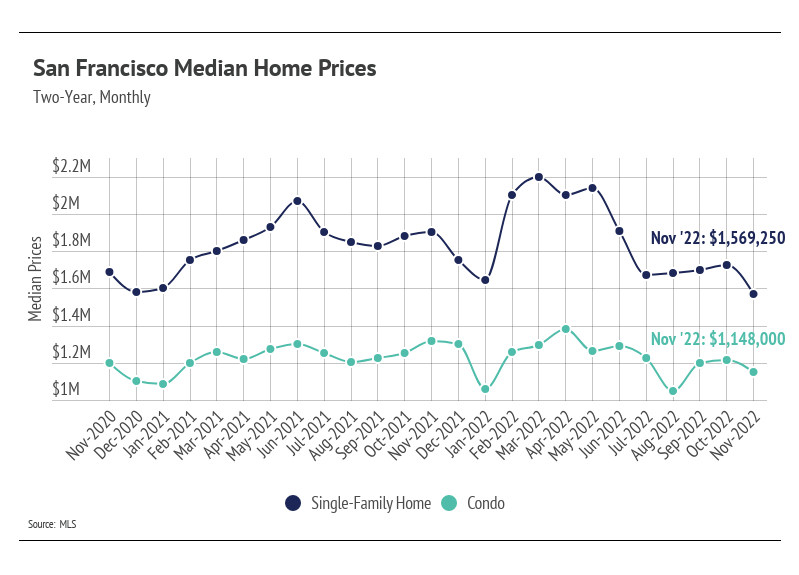

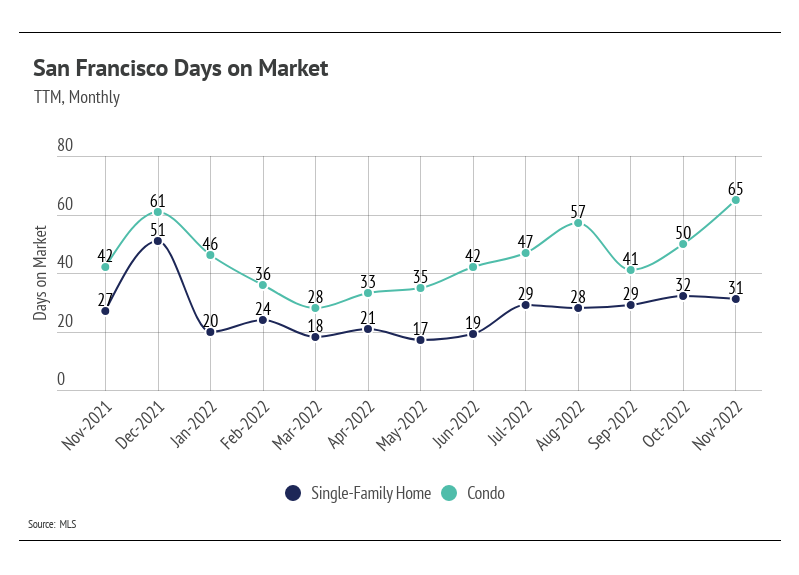

As we mentioned in the Big Story, the market is cooling on both the buy and the sell sides. When there are fewer sellers, there are also fewer buyers, because some buyers are selling their homes to move to others in the same market. New listings have declined faster than sales, causing inventory to decline near the historically low level we experienced last winter. However, the key difference is that fewer buyers are on the market — so, even with low inventory, buyers can still find the home that’s right for them. The low inventory has insulated prices from a major reversal. Single-family home prices have declined 29% from the March peak, which matches remarkably well with the increasing cost of a loan due to the rate increases. Not that you would or could finance the whole cost of the $2.2 million median home at 3.5% in March, but the cost of a $2.2 million mortgage at 3.5% is essentially the same as the cost of November’s $1.56 million median-priced home at 6.5%. Condo prices haven’t declined as significantly as single-family homes, down 17% from the April peak.

Moving forward, prices will likely contract slightly more through the winter, which is typical. Without any signs of interest rates dropping, we’re entering a stage of slower, longer-term growth — but still growth. In the short term, however, prices may come down a little more. Real estate has shown itself to be one of the best investments in recent history and is, on average, the largest store of wealth for an individual or family. Price appreciation will likely move to a more normal growth rate of around 5-6% in the coming years, which makes for a much healthier market than what occurred in 2020 and 2021.

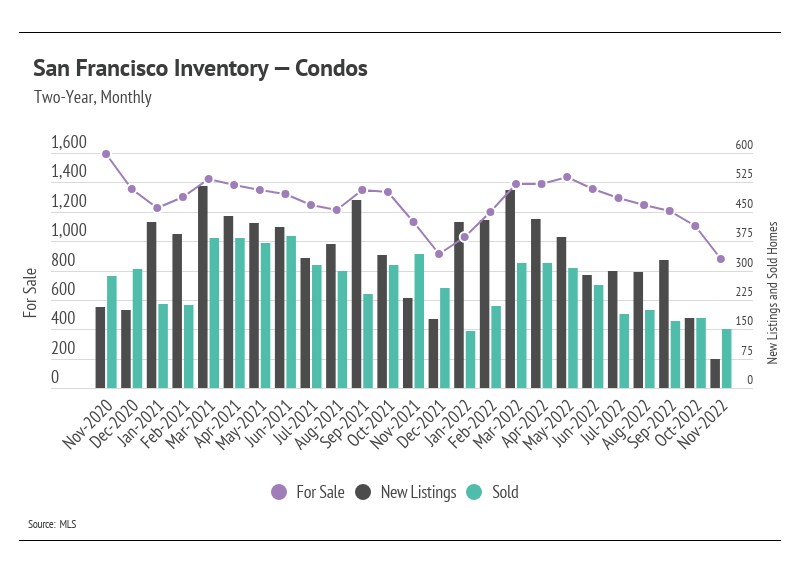

Inventory continues to decline, following seasonal trends

San Francisco, along with the rest of the country, has not returned to anywhere near pre-pandemic inventory levels after the buying boom last year. Inventory in 2022 failed to accumulate meaningfully throughout this year. We can compare sales and new listings from 2021 to 2022 to see the effects of fewer homes coming to market. Fewer homes and the rising rate environment have dropped demand. Softening demand has brought the market back to a sellers’ market for single-family homes and toward balance for condos despite declining inventory.

Months of Supply Inventory shows the market shifts even with declining inventory

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). MSI trended higher (away from a sellers’ market) in the spring and summer before inventory began to decline due to steady sales and a drop in new listings. The lack of inventory for single-family homes and condos has driven MSI lower, indicating the market favors sellers for single-family homes and is near balance for condos.

Local Lowdown Data

If you are interested in selling, buying or just curious about the

San Francisco and Bay Area real estate market, please give me a call.

We are here to help you and anyone you care about.